Categories

Case studies on First to Market use proprietary Category Signals to study timing, market maturity, competitive density, positioning patterns, funding activity, and buyer readiness across emerging markets.

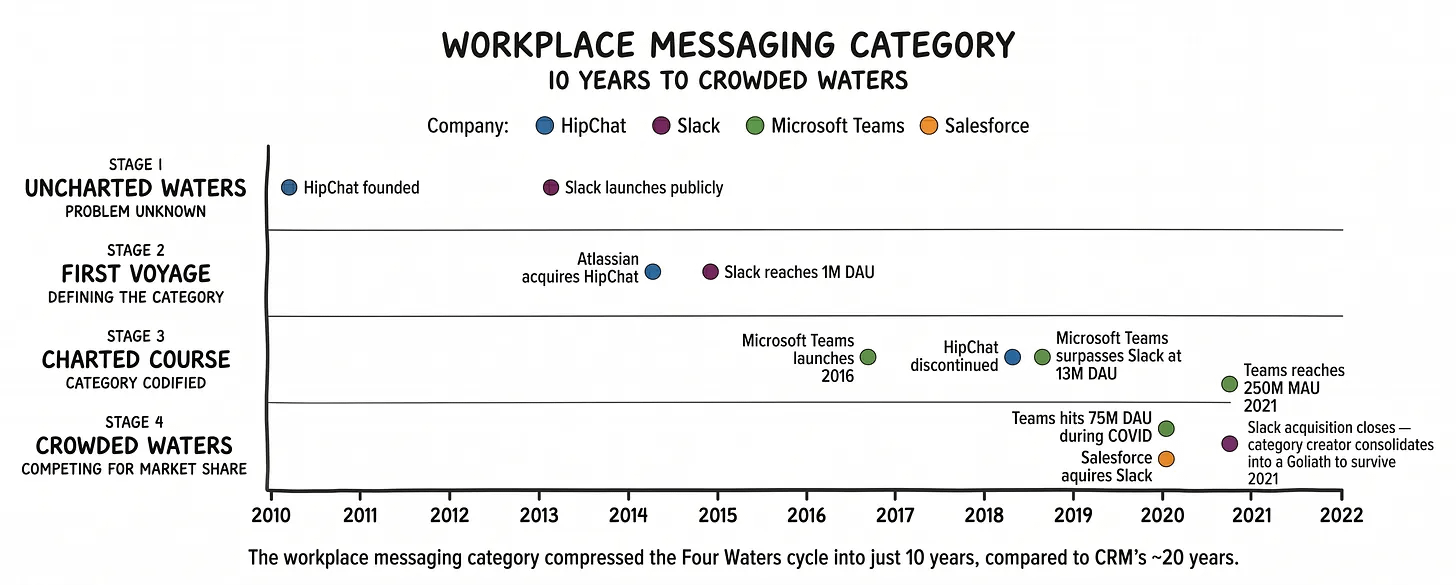

Contact research@garberson.com if you would like a readout on any of the actively monitored categories.

We map each category across 51 signals and incumbents/challengers in each category across 102 signals to analyze:

Category origin and history

Market maturity and timing

Competitive density

Funding and acquisition patterns

Analyst/review-site recognition

Positioning patterns

Product and buyer readiness

Signs that a category is opening, consolidating, or being redefined

The full research is not published as a database, but selected findings appear in weekly posts.

Applicant Tracking Systems (ATS)

ATS is a settled 30-year-old category at $3.28B and continuing to grow slowly, with entrenched incumbents in iCIMS, Oracle's Taleo, and SAP SuccessFactors.

By the Four Waters read it sits in Crowded Waters: buyers comparison-shop, the most common complaint is that legacy platforms are rigid compliance engines recruiters work around rather than with, and consolidation is underway.

What makes it interesting is that the majority of companies now use AI in recruiting, and agentic tools are moving from keyword parsing to end-to-end sourcing, screening, and interviewing.

The question is whether AI reset a compliance-bound category or if the HR platforms (e.g. Workday, Rippling) can absorb hiring back into the platform.

CRM

CRM is a mature category. The term was coined around 1995, the name is fully settled, and it's now an $82–99B global market with hundreds of competitors and 12+ unicorns.

The textbook play at this stage is to optimize and consolidate, not reinvent, which is exactly what the best-funded challengers are betting against. AI is the crack in the wall: nearly a third of Salesforce customers are reportedly weighing alternatives, and AI-native entrants like Attio and Sequoia-backed Day AI are raising on the premise that "agentic CRM" resets the category rather than just bolting features onto it.

The question still being debated: Is AI a genuine category reset, or just the next feature war the incumbents win on distribution?

Meeting Assistants

The meeting assistant category is young but moving fast. Otter claimed the name around 2018, and it's already a $3.47B market growing +20% a year, with two fresh unicorns (Fireflies and Granola).

By the Four Waters read it's mid-land-grab in Charted Course: Gartner started covering it in 2024, adoption is overwhelmingly bottom-up and product-led, and challengers are racing to define the category before it settles.

The real question is whether it survives as a standalone category or becomes a feature that Zoom, Microsoft, Notion and Google absorb into the meeting itself.

Legal Research

A 50-year duopoly is finally being disrupted. Westlaw (Thomson Reuters) and LexisNexis have owned legal research since the 1970s with a moat of proprietary content.

By the Four Waters read the AI-native layer is in a fast Charted Course land grab: Harvey reached $11B in 2026, with Legora and Eve close behind, and legal AI software is projected to continue growing.

The defining shift is natural-language Q&A and automated drafting replacing basic search, but the incumbents are acquiring and partnering to be competitive. The unresolved tension is whether content licensing or AI capability is the real moat now: challengers have the better interface, but incumbents own the authoritative corpus and the law-firm distribution.